Manufactured Home Foundation Certificate: What Lenders Need

- Matt Cameron

- Jun 12

- 9 min read

A Manufactured Home Foundation Certificate is a licensed engineer’s or architect’s sealed statement confirming that a manufactured home sits on a permanent foundation meeting the standards set by the 1996 HUD Permanent Foundations Guide for Manufactured Housing. Lenders require this document before approving FHA, VA, USDA, or most conventional loans on a manufactured home. Without it, your home is classified as personal property rather than real estate, and your financing options shrink considerably. Understanding what lenders are looking for in a manufactured home foundation certificate puts you in control of the process before problems surface at closing.

What lenders require from a manufactured home foundation certificate

Foundation certification is a non-discretionary underwriting requirement. A lender will deny your loan regardless of your credit score, income, or down payment if this document is missing. That is not a technicality. It is a hard stop in the underwriting process for FHA, VA, USDA, and most conventional loan programs.

The certificate itself is a sealed letter from a licensed structural engineer or architect. It states that the home’s foundation was inspected and found to comply with the HUD Permanent Foundations Guide for Manufactured Housing, published in 1996. That guide sets the minimum standards for foundation type, anchoring systems, and installation quality that mortgage programs recognize as qualifying a home for real estate financing.

Here is why the loan type matters so much to you as a buyer:

FHA loans require foundation certification under HUD guidelines. The home must be on a permanent foundation, and the engineer’s letter must be on file before underwriting closes.

VA loans follow the same requirement. The Department of Veterans Affairs will not guarantee a loan on a manufactured home that lacks a compliant permanent foundation and the corresponding certificate.

USDA Rural Development loans also mandate certification. The home must meet HUD standards and be titled as real property in the county where it sits.

Conventional loans through Fannie Mae and Freddie Mac require the home to be on a permanent foundation and classified as real estate. The engineer’s certification is the document that confirms both conditions are met.

Chattel loans, which treat the home as personal property, do not require foundation certification. However, chattel loan rates average around 9.5%, compared to mortgage rates that are typically several points lower, and loan terms are shorter.

The financing gap between a certified home and an uncertified one is significant. Only 44% of manufactured homes are financed with mortgages, compared to 95% of site-built homes. That gap exists largely because so many manufactured homes either lack permanent foundations or have not been certified. Buyers who secure certification before applying for a loan access better rates, longer terms, and more competitive programs.

Pro Tip: Ask your lender which specific loan program you are applying for and confirm in writing that foundation certification is required before you order the inspection. This prevents surprises and keeps your timeline on track.

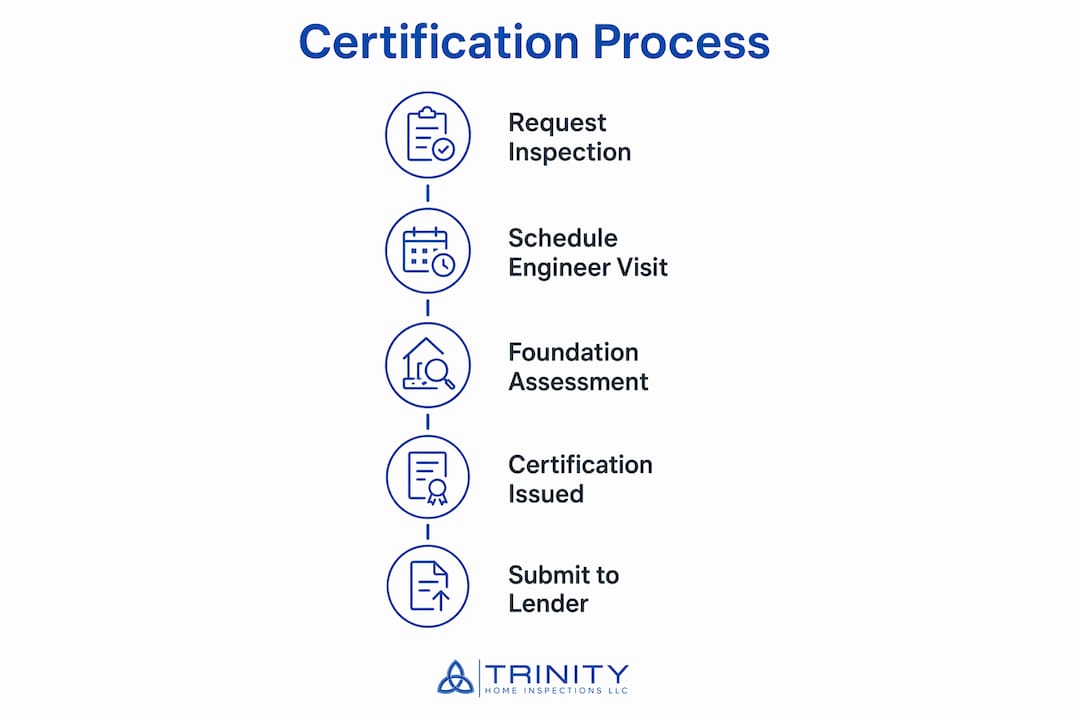

How the foundation certification process works

The certification process follows a defined sequence, and knowing each step helps you avoid delays.

Hire a licensed structural engineer or architect. The professional must be licensed in the state where the home is located and must have experience with manufactured housing standards. Not every structural engineer is familiar with the 1996 HUD Permanent Foundations Guide, so confirm their background before scheduling.

Schedule the site inspection. The engineer visits the property and physically inspects the foundation, anchoring systems, and installation. This is not a desktop review. The inspector needs direct access to the crawlspace or under-home area to verify what is actually there.

Foundation type is evaluated. The HUD guide recognizes several compliant foundation types, including concrete perimeter walls, concrete piers, and concrete slab systems. The engineer confirms which type is present and whether it meets the minimum specifications for the home’s size and weight.

Anchoring systems are checked. Certification inspections include a detailed review of the tie-down and anchoring hardware that secures the home to the foundation. Corroded, missing, or improperly installed anchors are common reasons a home fails initial certification.

HUD labels are verified. Every manufactured home built after June 15, 1976 carries a HUD certification label on the exterior and a HUD Data Plate inside. The engineer confirms these labels are present and legible. If they are missing, the certification process stops until the issue is resolved.

The engineer issues a sealed letter. If the foundation passes inspection, the engineer produces a signed and sealed letter stating compliance with the HUD Permanent Foundations Guide. This letter goes to your lender as part of the loan file.

Re-inspection if deficiencies are found. If the foundation does not meet standards, the engineer documents what needs correction. Once repairs are made, a follow-up inspection is scheduled before the letter is issued.

The typical cost for certification ranges from $400 to $700 for a standard single-section home. Multi-section homes or properties with complex terrain or difficult access can push costs higher. You can review a detailed breakdown of what affects pricing on the foundation inspection cost page. Budget for this expense early in your purchase timeline, not as an afterthought the week before closing.

Pro Tip: Order the foundation certification at the same time you order your general home inspection. Running both simultaneously saves time and gives you a complete picture of the home’s condition before you are locked into a closing date.

Common hurdles that cause certification delays

Most delays in the certification process come from a short list of predictable problems. Knowing them in advance gives you the best chance of avoiding them.

Blocked crawlspace access. Inspectors cannot certify a foundation if the anchoring systems are not physically accessible and visible. Skirting that is sealed shut, stored items blocking the crawlspace opening, or additions built over access panels all create this problem. Before the engineer arrives, confirm that the crawlspace has a clear, unobstructed entry point.

Missing or illegible HUD labels. Replacement of missing HUD Data Plates can take weeks or may be impossible for older homes. If the label is gone, the lender has no way to confirm the home was built to federal standards. Buyers should verify label existence before making an offer on a manufactured home, not after going under contract.

Non-compliant additions. Porches, room additions, and attached structures built after the original installation can complicate certification. If an addition was built over part of the foundation or altered the anchoring system, the engineer must evaluate whether the modification affects compliance. This often requires additional review time and sometimes structural corrections.

Outdated or deteriorated anchoring hardware. Older homes may have tie-down straps or anchor hardware that has corroded or loosened over time. The engineer will flag these during inspection, and the seller or buyer will need to arrange repairs before certification can be completed.

Foundation type that does not meet HUD standards. Some older manufactured homes were placed on stacked blocks or wood piers that do not qualify as permanent foundations under the 1996 HUD guide. In these cases, the foundation itself must be upgraded before certification is possible.

Pro Tip: Use the foundation inspection checklist to walk through the home before the engineer arrives. Catching access issues or visible anchor problems early gives you time to address them without delaying your loan.

The earlier you initiate the certification process, the less risk you carry of a last-minute loan denial. Buyers who wait until the final weeks before closing leave themselves no room to correct problems that could have been resolved in a matter of days with proper planning.

How the certificate legally connects your home to the land

The foundation certificate does more than satisfy a lender’s checklist. It is the legal mechanism that converts a manufactured home from personal property to real estate. That distinction controls which loan programs you can access and what your long-term ownership looks like.

Status | Classification | Financing available | Typical rate |

No permanent foundation | Personal property (chattel) | Chattel loans only | ~9.5% or higher |

Permanent foundation, no certificate | Unclear classification | Limited options, lender dependent | Varies |

Permanent foundation with certificate | Real property | FHA, VA, USDA, conventional | Standard mortgage rates |

Real property title recorded | Full real estate | All mortgage programs | Best available terms |

A manufactured home must be on owned land and set on a permanent foundation to qualify as real property for mortgage financing. Renting the land under the home, even with a long-term lease, typically disqualifies the home from FHA, VA, and USDA programs. You must own the land outright or be purchasing it simultaneously with the home.

Once the foundation certificate is in place, the next step is retiring the manufactured home title. In Alabama, this means filing with the county probate court to remove the personal property title and record the home as real estate attached to the land. The process requires the certificate, proof of land ownership, and documentation that the home is permanently affixed. After the title is retired, the home is treated the same as any site-built property for financing and tax purposes.

Foundation certification enables lenders to make this legal conversion official. Without the certificate, the title retirement process cannot be completed, and the home remains personal property regardless of how it looks physically. Lenders see the permanent foundation as the mechanism legally linking home to land, which is why the certificate carries as much legal weight as it does physical significance.

If you are buying a manufactured home where the seller has not yet retired the title, factor that timeline into your closing schedule. Title retirement after certification typically takes two to four weeks depending on the county. In Baldwin, Mobile, and Escambia counties in Alabama, the probate process is well established for manufactured homes, but it still requires lead time.

Key takeaways

A manufactured home foundation certificate is the single document that determines whether your home qualifies for real estate mortgage financing or is limited to higher-rate chattel loans.

Point | Details |

Certificate is mandatory for most loans | FHA, VA, USDA, and conventional loans all require a licensed engineer’s sealed foundation letter. |

Missing certificate means higher costs | Without certification, chattel loans averaging around 9.5% become the primary financing option. |

Start certification early | Ordering the inspection at the start of the purchase process prevents last-minute closing delays. |

HUD labels must be verified first | Missing or illegible HUD Data Plates can stop certification entirely and take weeks to resolve. |

Land ownership is required | The home must sit on land you own for the certificate to support real property classification. |

What I’ve learned about foundation certification after inspecting manufactured homes across the Gulf Coast

I have walked under a lot of manufactured homes in Baldwin, Mobile, and Escambia counties. What surprises buyers most is not the cost of certification or the timeline. It is how often a home that looks perfectly fine from the outside has a crawlspace that no engineer can certify without significant preparation work.

The most common situation I see is skirting that has been sealed so tightly that there is no practical way to access the crawlspace without removing panels. Sellers often do not realize this is a problem because the home has been sitting on that foundation for years without anyone needing to get underneath it. The moment a buyer applies for an FHA or VA loan, that access issue becomes a real obstacle.

The second thing buyers consistently underestimate is the HUD label requirement. I have seen deals fall apart because a label was painted over during a renovation or removed during a skirting replacement years before the current owner bought the home. Replacing a missing HUD label is not a quick fix. It involves contacting the Institute for Building Technology and Safety, submitting documentation, and waiting. For older homes, replacement may not be possible at all.

My honest advice is this: if you are buying a manufactured home and planning to finance it with anything other than a chattel loan, treat the foundation certification the same way you treat the home inspection. Order it early, attend it if you can, and do not assume the home will pass just because it looks solid. The manufactured home engineering certification process rewards buyers who prepare and penalizes those who wait.

The good news is that most foundation issues are correctable. A failed initial inspection is not the end of the deal. It is a list of repairs that, once completed, puts you right back on track for the loan you want.

Get your foundation inspection right the first time with Trinity Home Inspections

Trinity Home Inspections works with homebuyers across Baldwin, Mobile, Escambia, and surrounding Alabama counties to prepare manufactured homes for the certification process. Our InterNACHI-certified inspectors understand what lenders are looking for and can identify access issues, anchor concerns, and documentation gaps before the engineer arrives. Getting these details right early protects your financing and your timeline. Call us at 251-210-7376 or visit TrinityInspectionsLLC.com to schedule your inspection today.

FAQ

What is a manufactured home foundation certificate?

A manufactured home foundation certificate is a sealed letter from a licensed structural engineer or architect confirming that the home’s foundation meets the 1996 HUD Permanent Foundations Guide for Manufactured Housing. Lenders require this document to classify the home as real estate and approve FHA, VA, USDA, or conventional mortgage financing.

How much does foundation certification cost?

The standard cost for certification ranges from $500 to $550, covering the site inspection and the engineer’s sealed letter.

Can a manufactured home fail foundation certification?

Yes. Common reasons for failure include non-compliant foundation types, corroded or missing anchoring hardware, blocked crawlspace access, and missing HUD labels. Most issues are correctable, and a re-inspection can be scheduled once repairs are completed.

Do I need to own the land for the certificate to matter?

Yes. The foundation certificate supports real property classification only when the home sits on land you own. If you lease the land, most FHA, VA, and USDA programs will not qualify the home for mortgage financing regardless of the foundation’s condition.

How long does the certification process take?

Most certifications are completed within one to two weeks from the initial inspection, assuming no deficiencies are found. If repairs are needed, the timeline extends based on how quickly corrections are made and when the engineer can return for re-inspection.

Recommended