IBHS FORTIFIED certificate: unlock real home value

- Matt Cameron

- May 5

- 11 min read

When a Category 2 hurricane rolls across the Gulf Coast, the difference between a home that survives mostly intact and one that suffers catastrophic damage often comes down to a single document most buyers never think to ask about. The IBHS FORTIFIED designation certificate is not a marketing label or a builder’s badge. It is a verified, third-party confirmation that a home was constructed or upgraded to withstand the specific wind and storm conditions common to Gulf Coast Alabama. For buyers and sellers in Baldwin County, Mobile County, and the surrounding areas, understanding this certificate can mean the difference between real negotiating leverage and leaving serious money on the table.

Key Takeaways

Point | Details |

FORTIFIED beats code | Designated homes perform significantly better in storms than code-minimum builds. |

Certification process matters | Proper inspection, documentation, and regular renewal are vital for valid, leveraged certificates. |

Prevents costly mistakes | Knowing the technical and paperwork edge cases avoids delays or loss of certification. |

Boosts negotiation power | Buyers and sellers both benefit from transparent, FORTIFIED evidence in transactions. |

What is the IBHS FORTIFIED designation certificate?

The Insurance Institute for Business and Home Safety (IBHS) created the FORTIFIED program to address a problem that building codes alone cannot solve: minimum standards are not the same as real protection. Building codes establish a floor, the least a home must meet to be legally habitable. FORTIFIED raises that floor significantly, requiring documentation, third-party verification, and proven installation methods rather than just a set of construction drawings stamped approved.

A FORTIFIED designation certificate is the official document confirming that a specific home has been evaluated by a certified FORTIFIED Evaluator and meets the program’s published standards. It is property-specific, owner-transferable, and time-limited. For Gulf Coast buyers, it represents documented evidence of a home’s storm-resilient construction, not just a seller’s word or a marketing claim.

The 2025 FORTIFIED Home Standard establishes three certification levels that build on each other:

FORTIFIED Roof: The base level. It requires a sealed roof deck, specific roofing materials, and proper attachment to reduce the most common and costly source of storm damage: roof failure. This is the starting point every home must achieve before advancing.

FORTIFIED Silver: Builds on the Roof level by adding protection for openings such as windows, doors, skylights, and the garage door, along with chimney upgrades where applicable. Openings are frequently where water and wind enter a damaged structure.

FORTIFIED Gold: The highest level, requiring a continuous load path that ties the roof structure to the walls and the walls to the foundation. This structural connection is what keeps a home from “unzipping” under sustained high winds.

These levels are cumulative, meaning you cannot achieve Silver without first earning Roof, and Gold requires both Roof and Silver to be in place. The program is available to single-family detached homes built after 1994 in hurricane and high-wind zones, which makes the Gulf Coast Alabama market an ideal candidate.

“FORTIFIED certification is not just a renovation checklist. It is a documented chain of evidence that the right materials were installed the right way, verified by someone trained specifically to evaluate it.”

For sellers, holding a current FORTIFIED certificate immediately separates your listing from comparable homes. For buyers, it provides concrete assurance about what you are actually purchasing. Our detailed Alabama FORTIFIED homes guide covers the upgrade paths in more depth if you are considering pursuing or requiring designation in a transaction.

How the FORTIFIED certification process works in Alabama

With a clear view of the FORTIFIED certificate’s value, here is exactly how the process unfolds for Gulf Coast homes and what to expect at each step.

The certification process is systematic, but it has specific requirements that can trip up homeowners who are not prepared. Understanding each step before you start saves time, money, and frustration.

Hire a certified FORTIFIED Evaluator. Only evaluators certified through IBHS are authorized to perform FORTIFIED inspections and issue certificates. You can find a current list on the IBHS website. This is not a job for a general contractor or a standard home inspector acting outside their certification.

Pre-inspection documentation review. Before any physical inspection, the evaluator will review existing documentation including original construction permits, manufacturer product data sheets for roofing materials, and any prior repair or replacement records. If this paperwork is missing or incomplete, the process stalls here.

Physical inspection of the home. The evaluator visits the property and inspects the roof covering, roof deck attachment, roof-to-wall connections, openings, and structural connections depending on the target designation level. Photographs are taken at specific points as part of the evidence package.

Documentation submission. All photos, product data sheets, permit records, and the evaluator’s findings are submitted to IBHS for review. This is where incomplete documentation causes the most delays.

IBHS review and certificate issuance. IBHS reviews the submission package. If everything is in order, the designation certificate is issued and the property is registered in the FORTIFIED database, which insurers can query directly.

Renewal at the five-year mark. According to the 2025 FORTIFIED Home Standard, FORTIFIED certificates expire after 5 years from issuance and require renewal via a re-designation inspection by a certified FORTIFIED Evaluator, focusing on the roof and any changes made since the last evaluation.

Several things commonly delay or jeopardize the process. Missing manufacturer documentation for roofing materials is the most frequent issue. If a contractor replaced the roof without retaining product data sheets, you may need to tear into the installation to verify what was used. Unpermitted repairs or additions are another common stumbling block, particularly in older Gulf Coast neighborhoods where informal repairs after storm events are common.

Preparing your home’s paperwork well before you engage an evaluator makes a significant difference. Review home exterior maintenance tips specific to Gulf Coast conditions to understand what the evaluator will be looking at closely. You should also pull wind mitigation reports from prior inspections since they often contain the documentation the evaluator needs. If the roof has not been inspected recently, scheduling professional roof inspections before the FORTIFIED evaluation helps surface any issues you can address in advance.

Pro Tip: Take dated photographs of every roofing and opening upgrade you make, even routine ones. Store them digitally alongside the contractor invoices and product data sheets. When renewal time comes around, having this organized file ready can cut the re-designation timeline significantly and reduce the evaluator’s on-site time.

How FORTIFIED homes outperform standard construction

So what difference does certification make when storms actually hit? Let’s look at hurricane-tested results that matter to buyers and sellers.

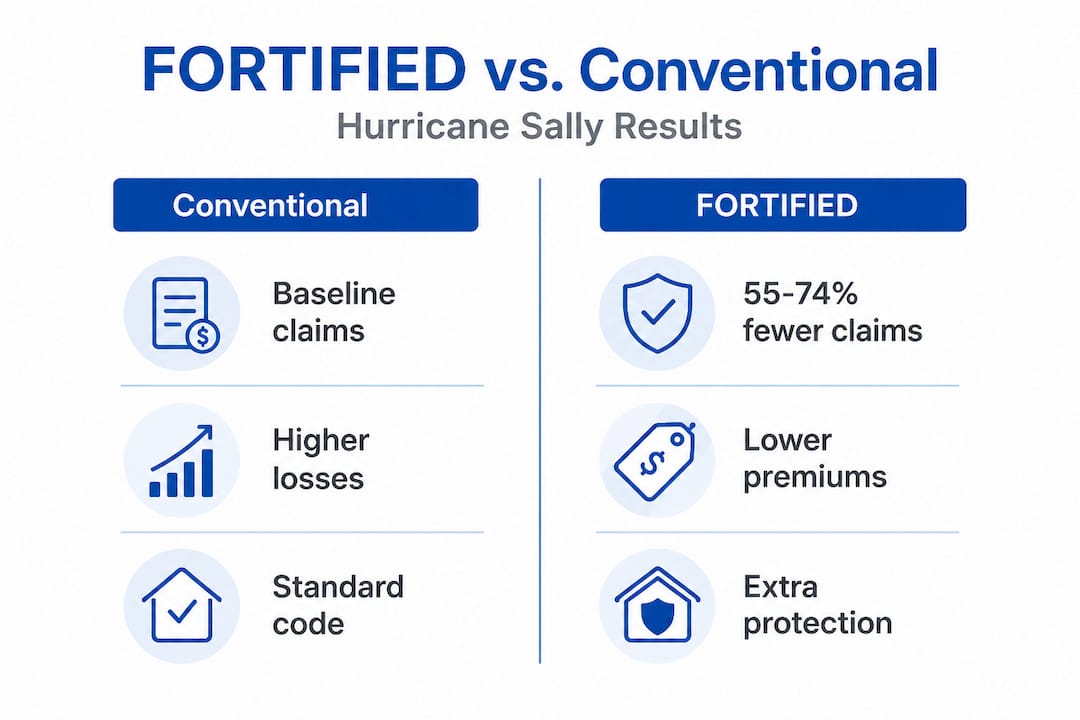

The most compelling evidence for FORTIFIED’s real-world value comes from Hurricane Sally, a Category 2 storm that made landfall near Gulf Shores, Alabama in September 2020. This event gave researchers and insurers a rare opportunity to compare FORTIFIED and non-FORTIFIED homes in the same geographic area under identical storm conditions.

The results were striking. According to the Alabama DOI’s post-Sally performance analysis, FORTIFIED homes showed 55 to 74 percent fewer insurance claims, 15 to 40 percent lower claim severity, and 51 to 72 percent lower loss ratios compared to conventional homes. These are not projections. They are real claim outcomes from a real storm in this exact region.

What makes this data particularly significant for Gulf Coast buyers is a detail that goes deeper. The same study confirms that FORTIFIED outperformed even code-similar homes that did not carry the designation. In other words, homes built to the same general construction standards but without the FORTIFIED documentation and third-party verification performed notably worse. That gap points directly to the importance of installation quality and evaluation rigor, not just materials selected.

Here is a direct comparison to help you visualize what that means in practice:

Metric | Conventional homes | FORTIFIED homes |

Claim frequency | Baseline | 55 to 74% lower |

Claim severity | Baseline | 15 to 40% lower |

Loss ratio | Baseline | 51 to 72% lower |

Insurer savings (Roof level) | N/A | $105.6 million |

Insurer savings (Gold level) | N/A | $116.1 million |

The insurer savings translate directly into lower premiums for homeowners. Alabama’s insurance market has been tightening significantly in coastal areas, with several carriers restricting coverage or raising rates. A FORTIFIED designation provides measurable relief by giving insurers documented evidence that the home carries substantially reduced risk.

The specific elements that explain this performance gap are worth understanding. Sealed roof decks prevent water infiltration when shingles are lost. Enhanced fastener patterns keep the roof covering attached longer in sustained winds. Verified continuous load paths prevent the catastrophic structural separations that create total losses. The difference is not theoretical. It shows up in real claim data.

For buyers considering tornado resistant house design features or wondering about hurricane impact windows, the FORTIFIED program provides a framework where all those individual upgrades are evaluated and documented together rather than in isolation. This is important because building code performance research consistently shows that code compliance alone does not predict storm performance the way documented, verified construction does.

Key requirements and edge cases for FORTIFIED designation

While the process is straightforward for most, a few technical and paperwork snags can trip up even experienced homeowners. Here is what to watch for in Alabama.

Most homeowners focus on the physical upgrades and underestimate the documentation burden. FORTIFIED is as much a paper trail as it is a construction standard. Missing even one required document, such as a product approval number for roofing materials or a photo of a specific installation detail, can halt the process entirely.

Here is a summary of the key documentation and physical requirements that commonly affect Gulf Coast transactions:

Requirement category | What is needed | Common problem |

Roof covering | Manufacturer product data, FL or ICC approval | Lost paperwork after contractor job |

Roof deck attachment | Fastener spacing photos taken during installation | Not documented if work was done informally |

Roof-to-wall connection | Strap specifications and installation photos | Missing for older repair work |

Openings (Silver/Gold) | Impact rating documentation for windows and doors | Common gap in pre-owned homes |

Structural load path (Gold) | Engineering documentation or manufacturer specs | Often requires professional preparation |

According to the 2025 FORTIFIED Home Standard, certain roofing materials and configurations can block or prevent designation entirely. Specifically, cement or clay hip-ridge tiles installed over asphalt in Gulf Coast applications may prevent a home from achieving FORTIFIED Roof designation. This matters because many Gulf Coast homes use tile accents that look attractive but create a documentation and compliance problem the seller may not discover until closing is near.

Key situations to watch for include:

Post-certification modifications: If you replace or modify the roof, add or replace windows, or make structural changes after receiving your certificate, those changes require verification before renewal. Undocumented post-certification work can cause you to lose the designation entirely at renewal time.

Missing installation photos: FORTIFIED requires photos taken during installation for specific elements like roof deck fastening and strap connections. Once the materials are covered over, you cannot recreate those photos. This means work done without a FORTIFIED Evaluator present may not qualify.

Multifamily and new construction: These property types use separate forms and evaluation criteria under the FORTIFIED program. If a seller is marketing a duplex or a brand-new build as FORTIFIED, verify that the correct designation category applies to that specific property type.

Unpermitted prior repairs: Gulf Coast homes frequently had storm repairs done quickly without permits after major events. These repairs may have used non-compliant materials or installation methods that cannot be verified retroactively.

The best way to protect yourself from these surprises is to pull common inspection findings data for your area and understand what typically gets flagged in Gulf Coast homes before you reach the FORTIFIED evaluation stage. Pay particular attention to the roof edge, since roof drip edge care is a frequently overlooked detail that affects both standard inspections and FORTIFIED compliance. A thorough pre-evaluation review from a roofing professional familiar with FORTIFIED requirements can surface these issues before they cost you a transaction.

Pro Tip: If you are selling a FORTIFIED-designated home, gather every document related to the designation into a single organized folder before listing. Include the original certificate, the evaluator’s report, all product data sheets, and photos from the installation. Providing this to a buyer’s agent upfront removes doubt and strengthens your negotiating position from the first showing.

The uncomfortable truth most buyers and sellers miss about FORTIFIED certification

Here is something worth saying plainly, even if it makes some people uncomfortable: meeting Alabama’s building code does not mean a home is ready for what the Gulf Coast regularly delivers.

Building codes are political documents as much as they are technical ones. They represent the minimum that the construction industry, local governments, and insurers negotiated at a specific point in time. Research on building code performance from Hurricane Ian in Florida confirmed what Sally data showed in Alabama: code-compliant homes still suffered significant damage, and the primary differentiator between damaged and undamaged properties was not the code level but the quality of installation and the presence of third-party documentation.

This matters enormously for how you approach a Gulf Coast transaction. We have seen buyers walk away from a FORTIFIED home because the seller priced it $8,000 above comparable listings, only to watch them close on a code-minimum house that required $22,000 in repairs after its first Gulf Coast storm season. The certificate looked like a premium. It was actually a discount on future risk.

For sellers, the FORTIFIED certificate is not just paperwork. It is negotiating leverage you can quantify. Lower insurance premiums are real and immediate. Reduced claim history protects your investment. And in a market where insurance availability on the Gulf Coast is genuinely constrained, a home with a documented lower risk profile is not just easier to insure. It is easier to sell to buyers who need financing, because lenders care about insurability.

What we encourage every buyer and seller to do goes beyond reviewing the certificate itself. Verify that the certificate is current, not expired. Confirm that no post-certification modifications were made without documentation. Ask whether the home’s current condition still reflects what was evaluated, since five years and a few storm seasons can change a roof’s condition substantially. The upgrades that prevent loss are only worth their value if the documentation supporting them is intact and current.

A FORTIFIED certificate tells you what the home was at the time of evaluation. A certified inspection tells you what it is right now. Both matter, and treating one as a substitute for the other is where buyers and sellers make the most costly mistakes we see in this market.

Enhance your Gulf Coast transaction with certified inspections

Understanding the FORTIFIED designation gives you a real advantage, but knowing what the certificate says and knowing what the home looks like today are two different things. A current, independent inspection closes that gap and gives you documented, photo-rich evidence of the home’s actual condition at the moment of sale.

[

At Trinity Home Inspections, we serve buyers and sellers across Baldwin, Mobile, Escambia, and surrounding Gulf Coast Alabama counties with InterNACHI-certified inspections that go beyond representative sampling. Our same-day reports include thermal imaging at no extra charge, video documentation of issues, and plain-English summaries that tell you what is urgent, what can wait, and what to budget for. You can start by running property and permit searches to verify a home’s history before your inspection date. Sellers ready to strengthen their listing can schedule a pre-listing home inspection that surfaces issues before buyers find them. When you are ready to move forward, connect with our local certified inspectors who know Gulf Coast homes and take every inspection as seriously as if it were our own family’s purchase.

Frequently asked questions

Who can issue an IBHS FORTIFIED designation certificate?

Only certified FORTIFIED Evaluators are authorized to inspect and issue or renew FORTIFIED designation certificates in Alabama. Verify your evaluator’s credentials directly through IBHS before scheduling.

How long is an IBHS FORTIFIED certificate valid?

FORTIFIED certificates are valid for 5 years from the date of issuance and must be renewed through a re-designation inspection by a certified FORTIFIED Evaluator.

What happens if I modify my home after getting the FORTIFIED certificate?

If you make changes such as roof updates or additions, those modifications require verification for FORTIFIED compliance, or you risk losing the designation at renewal time.

How does a FORTIFIED home affect insurance premiums in Alabama?

FORTIFIED homes often qualify for lower insurance premiums because they demonstrate 51 to 72 percent lower loss ratios and significantly reduced claim frequency compared to conventional construction.

Are there any home types or features that cannot get FORTIFIED certification?

Yes. Certain roofing configurations like cement or clay tiles over asphalt may prevent certification, and multifamily or new construction properties use separate forms with different evaluation criteria.

Recommended