Alabama FORTIFIED Homes Guide: Upgrades Save 50% Storm Loss

- Matt Cameron

- Apr 16

- 10 min read

Many Gulf Coast homes lack storm-resistant features despite high hurricane exposure.

FORTIFIED roofs meet stringent standards to reduce storm damage and lower insurance costs.

Proper certification and inspections ensure true resilience beyond building code minimums.

Gulf Coast Alabama homeowners sit in one of the most storm-exposed regions in the country, yet a surprising number of buyers and sellers have no idea whether their home can withstand the next major hurricane. FORTIFIED homes had 50% less loss severity during Hurricane Sally compared to standard code-built homes, according to Alabama Department of Insurance data. That gap is not a small margin. It represents real money, real safety, and real peace of mind. This guide walks you through the Strengthen Alabama Homes grant program, FORTIFIED Roof standards, the step-by-step application process, and how certified inspections tie it all together so you can make the most informed decision possible before buying or selling.

Key Takeaways

Point | Details |

SAH grants offer big savings | Eligible homeowners can receive up to $10,000 for wind mitigation upgrades in Alabama’s Gulf Coast. |

FORTIFIED roofs outperform standard | Homes with FORTIFIED roofs experienced up to 50% less storm damage than conventional properties. |

Inspections boost insurance and resale | FORTIFIED evaluation during inspection means possible 20-45% insurance discounts and higher sales prices. |

Certification process is strict | The SAH application and upgrade steps require quick action and precise compliance to secure grants and certification. |

Third-party verification is critical | Empirical studies prove FORTIFIED certification delivers more protection than basic building code compliance. |

Understanding the Strengthen Alabama Homes program

The Strengthen Alabama Homes (SAH) program is a state-funded initiative designed to help Gulf Coast homeowners upgrade their properties to meet FORTIFIED construction standards. The program is administered by the Alabama Department of Insurance and funded by the insurance industry, not taxpayer dollars. That distinction matters because it means the program has a direct financial interest in reducing storm losses, which keeps the funding sustainable year after year.

The SAH grant eligibility requirements are specific, and understanding them upfront will save you a lot of frustration. Here is what you need to qualify:

The home must be owner-occupied and used as a primary residence

The property must be a single-family home (condos, townhomes, and mobile homes do not qualify)

The home cannot be listed for sale at any point during the application and upgrade process

The property must be located in one of the eligible Gulf Coast counties

That last point about not being listed for sale is one of the most common sources of confusion for sellers. If you are planning to sell, you need to complete the FORTIFIED upgrade process before listing, not during or after.

The SAH program offers grants up to $10,000 to cover the cost of wind mitigation upgrades. If the total project cost exceeds $10,000, the homeowner is responsible for the difference. Most basic FORTIFIED Roof upgrades fall within or close to this range, though costs vary based on roof size, materials, and existing conditions.

Application windows open three times per year: January, April, and July. Missing a window means waiting for the next one, so planning ahead is essential. The program has already delivered impressive results across the state.

SAH Program Milestone | Data |

Total retrofits funded | Over 8,700 homes |

Total grant dollars issued | Over $86 million |

Maximum grant per home | $10,000 |

Application windows | January, April, July |

Those numbers reflect real homes that are now better protected across Baldwin, Mobile, Escambia, and surrounding counties. The wind mitigation report benefits extend beyond just storm protection. They also include documented evidence of upgrades that can directly influence your insurance premiums.

Pro Tip: Each stage of the SAH process carries a strict 7-day action deadline. If you miss a deadline at any point, your application can be closed and you will need to reapply in the next available window. Set calendar reminders for every step.

What makes a FORTIFIED Roof: Standards and upgrades

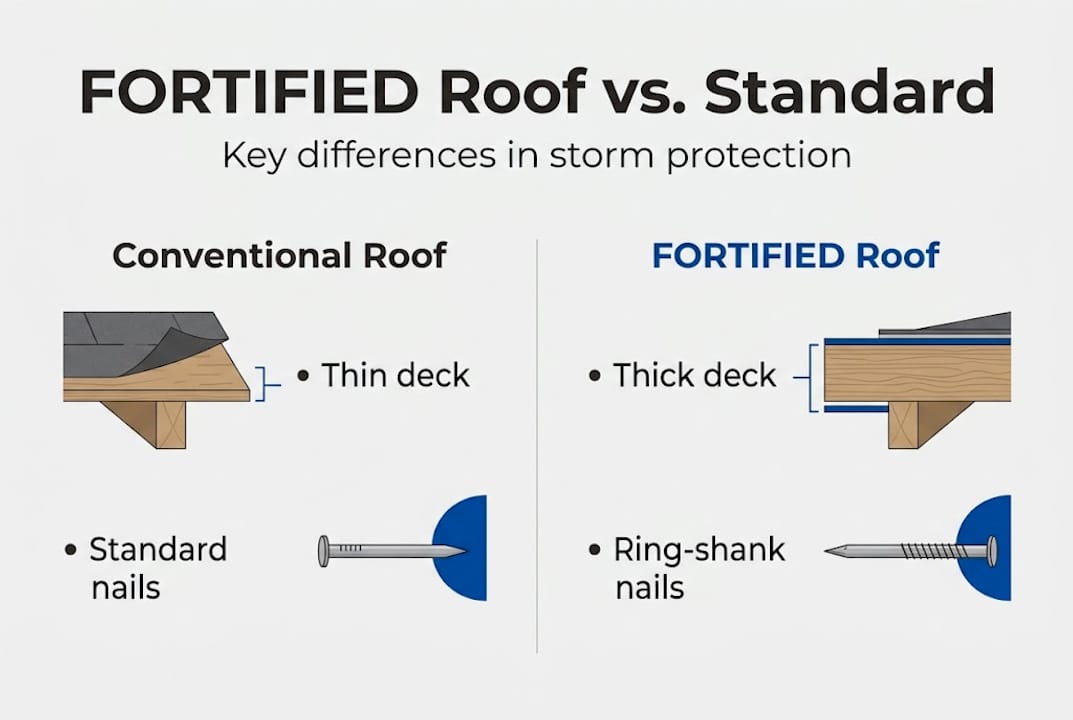

Not every new roof qualifies as a FORTIFIED Roof. The FORTIFIED Roof methodology is a specific set of construction standards developed by the Insurance Institute for Business and Home Safety (IBHS). These standards go well beyond Alabama’s minimum building code requirements, and that gap is exactly where most storm damage happens.

Here is what a FORTIFIED Roof requires:

Roof deck: Minimum 5/8-inch plywood or oriented strand board (OSB), with plywood preferred for Gulf Coast applications due to its superior moisture resistance

Nailing pattern: 8d ring-shank nails at 6 inches on center along edges and 12 inches in the field, which outperform standard smooth-shank nails in high-wind conditions

Secondary water barrier: Taped seams or spray foam adhesive applied to the roof deck to prevent water intrusion if shingles are lost during a storm

Roof covering: Must meet code-compliant wind resistance ratings for the applicable wind zone

Fasteners: All fasteners must be corrosion-resistant, which is a non-negotiable requirement for Gulf Coast homes exposed to salt air and humidity

The secondary water barrier is arguably the most important element. Standard roofs have no backup protection once shingles are torn off. A FORTIFIED Roof keeps rain out even after the outer layer is compromised, which is exactly what happened during Hurricane Sally when FORTIFIED homes performed so dramatically better.

Feature | Conventional Roof | FORTIFIED Roof |

Deck thickness | Varies, often 7/16-inch | Minimum 5/8-inch |

Nail type | Smooth-shank | 8d ring-shank |

Water barrier | None | Taped seams or spray foam |

Fastener type | Standard | Corrosion-resistant |

Wind resistance | Code minimum | Enhanced, tested standard |

Storm loss severity | Baseline | Up to 50% less |

For Gulf Coast buyers, this table tells a clear story. The difference between a conventional roof and a FORTIFIED Roof is not cosmetic. It is structural and performance-based. Reviewing home maintenance and FORTIFIED standards before you close on a property can help you understand what you are actually buying.

Sellers benefit from this knowledge too. If your home already has a FORTIFIED Roof, that is a marketable asset. If it does not, upgrading before listing could increase your sale price and attract buyers who understand the value of storm resilience. Reviewing essential home safety steps can help you prioritize which upgrades matter most before putting your home on the market.

Pro Tip: During any home inspection or pre-listing evaluation, ask specifically for FORTIFIED certification documents. A verbal claim that a roof was “built to FORTIFIED standards” is not the same as a verified certificate from IBHS.

SAH application and inspection: Step-by-step for buyers and sellers

The SAH process has multiple stages, and each one requires timely action. Here is the full sequence from start to finish:

Submit your online application through the SAH portal during an open window (January, April, or July)

Upload required documents including proof of ownership, insurance declarations page, and property information

Schedule an initial FORTIFIED inspection with a certified evaluator, which carries a $400 fee paid by the homeowner

Receive your initial evaluation report identifying what upgrades are needed to reach FORTIFIED Roof certification

Gather three contractor bids from SAH-approved contractors only (non-approved contractors disqualify the grant)

Submit bids and await grant award notification from the SAH program

Complete the approved upgrades using your selected contractor within the required timeframe

Schedule a post-work evaluation with your certified evaluator to verify the work meets FORTIFIED standards

Receive IBHS certification confirming your home’s FORTIFIED Roof status

The SAH application steps are clearly outlined on the program’s registration portal, but many applicants still run into problems. The most common mistakes include:

Missing the 7-day response deadline at any stage, which closes the application automatically

Hiring a contractor who is not on the SAH-approved list, which voids the grant

Failing the initial inspection due to pre-existing roof damage that was not addressed beforehand

Submitting incomplete documentation during the upload stage

“Third-party verification is what sets FORTIFIED homes above Alabama code-built properties.”

That verification comes from a certified FORTIFIED Evaluator, not just a contractor or a general inspector. The role of inspector certification is critical here because the evaluator must be specifically trained and recognized by IBHS to issue a valid certificate.

Once issued, the FORTIFIED certificate is valid for five years. After that, a reinspection is required to maintain certification status. For buyers, this means you need to check not only whether a home has a FORTIFIED certificate but also when it was issued and whether it is still current. Following inspection best practices during your due diligence period will help you catch these details before closing. Understanding how inspections protect homebuyers in this context goes beyond the standard checklist and into verified storm resilience.

How FORTIFIED evaluations enhance regular home inspections

A standard home inspection and a FORTIFIED evaluation are two different things, but they work best together. A home inspector assesses the overall condition of a property, covering everything from the foundation to the roof, electrical systems, plumbing, and more. A FORTIFIED Evaluator focuses specifically on whether the roof assembly meets IBHS certification standards.

Here is how the two roles differ and complement each other:

Home inspector: Evaluates overall safety, function, and condition of the entire property

FORTIFIED Evaluator: Verifies specific roof construction details against IBHS standards for wind resistance certification

Combined assessment: Gives buyers and sellers a complete picture of both general property condition and storm resilience

For buyers, having both assessments done before closing is one of the smartest moves you can make in a Gulf Coast market. The importance of inspections goes beyond finding defects. It gives you documented evidence of a property’s actual condition and certified storm performance.

The financial benefits of FORTIFIED certification are well-documented. According to the ALDOI, homeowners with FORTIFIED certification can see insurance premium reductions of 20 to 45 percent depending on their carrier and coverage level. On a $2,000 annual premium, that is a savings of $400 to $900 every single year. Over ten years, that adds up to real money.

Resale value is another factor that often gets overlooked. Homes with FORTIFIED certification carry approximately a 7% price premium compared to similar non-certified properties. For a $300,000 home, that is $21,000 in added value. When you factor in the SAH grant covering up to $10,000 of the upgrade cost, the return on investment becomes very clear.

“FORTIFIED roofs kept rain out better during Hurricane Sally, demonstrating a measurable performance advantage over standard construction that buyers and sellers cannot afford to ignore.”

Coordinating with a FORTIFIED Home Standards certified evaluator alongside your home inspector ensures that no detail falls through the cracks. The value of an accredited inspector is amplified when they understand how to work alongside the FORTIFIED evaluation process. If you are still forming your list of questions before hiring, reviewing questions for Gulf Coast inspectors will help you separate professionals from those who are just going through the motions.

Pro Tip: Always ask for the FORTIFIED certificate during any home inspection on a Gulf Coast property. If the seller cannot produce one, ask when the roof was last replaced and whether it was built to FORTIFIED standards. Then verify it.

A fresh perspective: Why FORTIFIED certification matters more than code compliance

Here is something most real estate conversations miss entirely: building to code is the floor, not the ceiling. Alabama’s minimum building code tells contractors what they must do to legally construct a home. It says nothing about how that home will actually perform when a Category 2 hurricane pushes a 100-mile-per-hour wind gust across your roof.

FORTIFIED certification is different because it is based on empirical performance data, not just engineering assumptions. IBHS studies confirm that FORTIFIED homes outperform code-built homes in real storm events, and the verification comes from a third party with no financial stake in the outcome of the inspection.

“Third-party verification from IBHS is what separates true resilience from mere code compliance.”

We see buyers and sellers make the same mistake repeatedly. They assume a newer roof or a recent permit means the home is storm-ready. It does not. A roof can be brand new, permitted, and inspected by a local building official and still lack the secondary water barrier, the ring-shank nails, and the corrosion-resistant fasteners that make the real difference in a storm.

Sellers especially leave money on the table by not advertising FORTIFIED status. If your home is certified, that fact belongs in your listing description, your disclosure documents, and your negotiation conversations. It is a documented, third-party-verified asset that justifies a higher asking price and gives buyers confidence. Reviewing the wind mitigation report benefits before listing can help you frame that value clearly for potential buyers.

Pro Tip: If you are a seller with a FORTIFIED-certified home, include the certificate number and expiration date in your listing materials. Buyers who understand Gulf Coast risk will recognize the value immediately.

Connect with certified inspection and upgrade specialists

Now that you understand the FORTIFIED process, the SAH grant, and how evaluations work alongside home inspections, the next step is taking action with professionals you can trust.

At Trinity Home Inspections, we serve buyers and sellers across Baldwin, Mobile, Escambia, Washington, Monroe, and Clarke counties with InterNACHI-certified inspections, same-day reports packed with photos and video, and free thermal imaging. We understand the Gulf Coast market and the specific storm risks that come with it. Start by using our property and permit search to check a home’s permit history before you commit. If you are selling, a pre-listing home inspection can identify issues before buyers do and help you price with confidence. Visit Trinity Home Inspections to book your inspection and get the clarity you need to move forward.

Frequently asked questions

Who is eligible for the Strengthen Alabama Homes grant?

Owner-occupied single-family homes in eligible Gulf Coast counties that are not listed for sale during the process qualify for the SAH grant. Condos, townhomes, and mobile homes are excluded.

How does a FORTIFIED roof differ from a regular roof?

A FORTIFIED Roof uses stronger materials, including 5/8-inch plywood, 8d ring-shank nails, a secondary water barrier, and corrosion-resistant fasteners that standard roofs do not require.

What steps are required to get the SAH grant?

You must apply online during an open window, pass an initial FORTIFIED inspection, submit three contractor bids, receive grant approval, complete the upgrades, and obtain IBHS certification after a final evaluation.

How can buyers verify a home’s FORTIFIED status?

Ask the seller for the FORTIFIED certificate and confirm the certificate number and expiration date with IBHS. Request this documentation during your home inspection period before closing.

Recommended