4-Point Insurance Inspections: What Gulf Coast Buyers Need

- Matt Cameron

- Apr 10

- 9 min read

If you think a full home inspection is all you need to close a deal on Alabama’s Gulf Coast, you’re missing a critical piece of the puzzle. Insurance companies in Baldwin and Mobile Counties routinely require a separate, focused assessment before they’ll issue or renew a policy on older homes. A 4-point insurance inspection evaluates four critical home systems: HVAC, electrical, plumbing, and roof. Without it, your closing can stall, your policy can be denied, and your deal can fall apart. Here’s everything you need to know to stay ahead of it.

Key Takeaways

Point | Details |

Focuses on aging systems | A 4-point inspection checks the four systems with the highest risk and claim history in older Gulf Coast homes. |

Mandatory for insurance approval | Insurers require a 4-point inspection for homes 20-30+ years old to assess eligibility and rates. |

Quick, affordable process | Most 4-point inspections are visual, take less than an hour, and cost around $100-200 in Alabama’s Gulf Coast. |

Complements full inspections | A 4-point does not replace a full inspection; both are needed for peace of mind and insurance requirements. |

Proactive preparation saves money | Addressing flagged risks after the inspection can lower premiums and prevent delays in real estate closings. |

What is a 4-point insurance inspection?

After understanding the importance of inspections for real estate deals, let’s clarify exactly what a 4-point insurance inspection entails.

A 4-point insurance inspection is a focused, visual evaluation of the four home systems that insurers care about most. It is not a full home inspection. It does not cover every corner of the property. Instead, it zeroes in on the systems most likely to generate costly claims, giving insurers a snapshot of the home’s risk level before they agree to cover it.

According to a 4-point inspection checklist, the four systems assessed are:

HVAC (Heating, Ventilation, and Air Conditioning): Age, condition, and operational function of the heating and cooling equipment

Electrical: Panel type, wiring material, breaker condition, and known hazards like aluminum wiring or Federal Pacific panels

Plumbing: Pipe material, supply and drain lines, water heater age and condition, and visible signs of leaks

Roof: Age, material, condition, visible damage, and estimated remaining life

These four systems account for over 60% of claims in older homes, which is exactly why insurers single them out. A failing HVAC unit, outdated knob-and-tube wiring, or a roof past its useful life are all red flags that can drive up an insurer’s risk exposure significantly.

Here’s how the 4-point inspection compares to a full home inspection:

Feature | 4-point inspection | Full home inspection |

Scope | 4 systems only | Entire property |

Depth | Visual, age, and condition | Detailed function and safety |

Required by | Insurance carrier | Buyer or lender |

Report used for | Insurance approval | Purchase decision |

Time to complete | 30 to 60 minutes | 2 to 4 hours |

For detailed inspection steps on each system, reviewing what inspectors look for in each category helps you prepare your home before the appointment. The key home system checks that matter most to insurers often overlap with what buyers should know before committing to a purchase.

Why do insurers require 4-point inspections in Alabama’s Gulf Coast?

Now that you know what’s covered, here’s why insurers particularly insist on these assessments for Alabama coastal properties.

The Gulf Coast is not a typical real estate market. Homes here face salt air corrosion, hurricane-force winds, heavy rainfall, and intense heat cycles that accelerate wear on every major system. Insurers know this, and they price their risk accordingly. For homes 20 to 30 years old or older, the risk of system failure is high enough that carriers require documented evidence of condition before issuing a policy.

“It is required by insurers primarily for homes 20 to 30 or more years old to assess risk of failure in these systems, which account for over 60% of claims in older homes.”

In Baldwin and Mobile Counties, coastal zone requirements are similar to Florida’s insurance rules but vary by carrier. Some insurers require the inspection for any home over 20 years old. Others set the threshold at 25 or 30 years. A few carriers now require it for all homes in high-wind or storm-surge zones, regardless of age.

Here’s a quick look at when a 4-point inspection is typically required:

Scenario | Requirement |

New policy on a home 20 to 30 years old | Almost always required |

Policy renewal on an aging home | Commonly required |

Home sale in a coastal zone | Required by most carriers |

New construction (under 10 years old) | Rarely required |

A 4-point inspection is mandatory in these situations:

Applying for a new homeowner’s insurance policy on an older home

Renewing an existing policy when the home has aged into the required threshold

Purchasing a home in a high-risk coastal zone like Gulf Shores or Orange Beach

Refinancing when the lender requires proof of insurability

Insurers use the inspection as a low-cost screening tool. For a relatively small fee, they get a documented picture of the home’s biggest risk areas. It costs them far less than paying out a claim on a 30-year-old electrical panel that sparks a fire. For Alabama Gulf Coast insurance requirements, understanding the local rules before you list or make an offer puts you in a much stronger position. Preparing for insurance approval starts well before closing day.

How does a 4-point insurance inspection work in practice?

Understanding why you need the inspection, let’s break down how it actually happens when you schedule one.

The process is straightforward. A licensed inspector visits the property, evaluates the four systems visually, photographs everything relevant, and produces a report that goes directly to your insurance carrier. There is no pass or fail grade. The inspector documents what exists, and the insurer decides what to do with that information.

Here is what the process looks like from start to finish:

Schedule the inspection with a licensed local inspector who is familiar with Gulf Coast insurance carrier requirements

Inspector arrives and conducts a visual, non-invasive walkthrough of the HVAC, electrical, plumbing, and roof systems

Photos are taken of each system, including equipment labels, panel interiors, pipe materials, and roof surfaces

Age and condition are documented for each system, along with estimated remaining useful life

Report is completed and delivered, typically the same day, in a format your insurance carrier accepts

You submit the report to your insurer as part of the policy application or renewal process

The inspection typically takes 30 to 60 minutes for most homes. The inspection cost in 2026 on Alabama’s Gulf Coast generally runs between $75 and $250, with most homeowners paying in the $100 to $200 range depending on property size and location.

The inspector is not there to judge your home or tell you what to fix. They document what they see. If your roof is 18 years old and showing wear, that goes in the report. If your electrical panel is a brand flagged by insurers, that gets noted too. The insurer then decides whether to approve the policy, require repairs before approval, or adjust your premium based on the findings.

Pro Tip: If you are a seller, address any obvious system issues before the inspector arrives. A water heater that is past its expected lifespan or a visibly damaged roof section can flag your property as high risk. Fixing these items ahead of time can prevent delays and keep your sale on track.

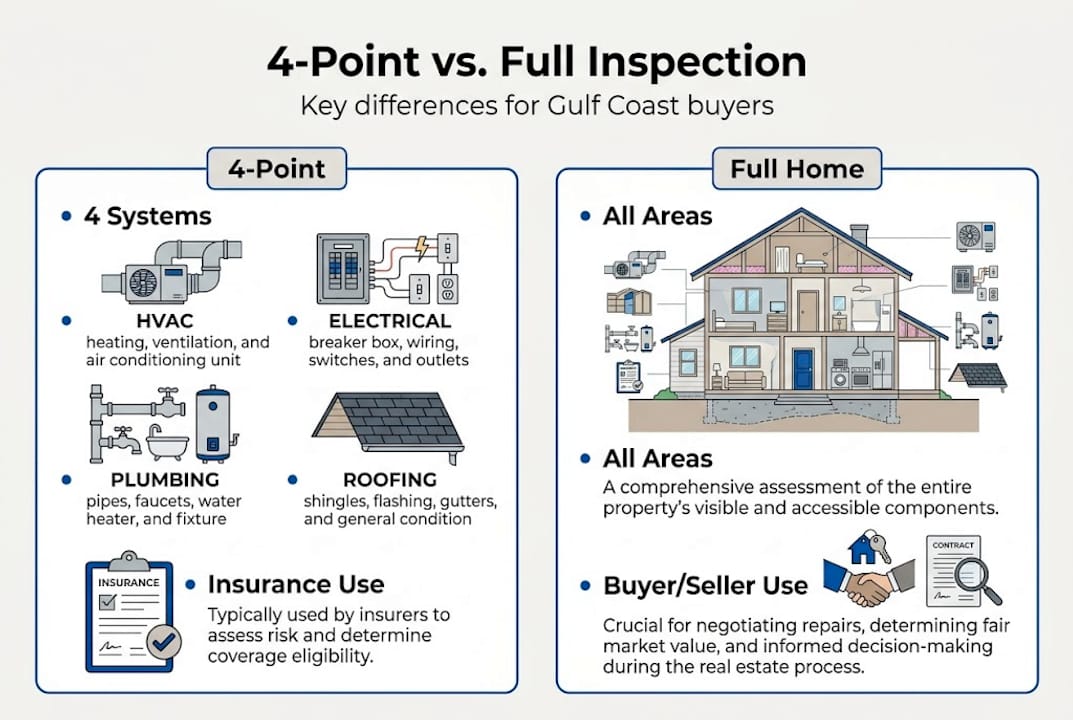

What’s the difference between a 4-point inspection and a full home inspection?

Since many buyers and sellers are uncertain about inspection types, here’s how the essential 4-point compares to the comprehensive full inspection.

These two inspections serve completely different purposes. Confusing them is one of the most common mistakes buyers and sellers make on the Gulf Coast. A full home inspection is for you, the buyer. It covers the entire property in detail, from the foundation to the attic, and helps you understand what you’re buying. A 4-point inspection is for your insurer. It covers only the four systems that drive the most claims.

Feature | 4-point inspection | Full home inspection |

Who requires it | Insurance carrier | Buyer, lender |

What it covers | HVAC, electrical, plumbing, roof | Entire home |

Outcome | Insurance approval or denial | Repair requests, negotiation |

Report validity | Single transaction | |

Pass or fail | No, flags risks only | No, identifies defects |

Key differences in what gets reported:

The 4-point report goes to the insurer and focuses on age, condition, and system type

The full inspection report goes to the buyer and covers safety, function, and maintenance needs

A 4-point report does not guarantee policy approval, it just provides the data the insurer needs

A full inspection can uncover issues the 4-point never touches, like foundation cracks or pest damage

For Gulf Coast transactions, you often need both. The benefits of full inspections extend well beyond insurance. They give buyers real negotiating power and a clear picture of what they’re getting into. The role during selling is equally important, as sellers who complete both inspections before listing tend to close faster and with fewer surprises. Understanding inspection report differences helps you use each document correctly in the transaction.

For homebuyers and sellers, pairing both inspections is the safest approach in any coastal Alabama real estate deal.

How to use 4-point inspection results for your real estate transaction

Finally, let’s put the inspection’s results into action and see how they guide closing and insurance on the Gulf Coast.

The report is not just a document you hand to your insurer and forget. It is a tool. Used correctly, it can protect your closing timeline, lower your insurance costs, and give you real leverage in negotiations.

If you are a buyer, here is how to use the results:

Submit the 4-point report to your insurance carrier immediately to start the policy approval process

Review flagged systems and request repairs from the seller before closing

Use documented system ages to negotiate price reductions if major replacements are imminent

Share the report with your lender if they require proof of insurability before finalizing financing

If you are a seller, your strategy is different:

Address flagged items before listing to avoid delays once a buyer’s insurer reviews the report

Keep your 4-point report current so it doesn’t expire mid-transaction

Use a clean report as a marketing tool to show buyers the home is insurable without complications

Pro Tip: Repairing or replacing a flagged system before the inspection, like upgrading an outdated electrical panel, can directly reduce your insurance premium. On the Gulf Coast, where premiums are already elevated due to storm risk, that savings adds up quickly.

In Alabama’s coastal market, insurance carriers may deny coverage or add surcharges for homes with flagged systems. A proactive approach, getting both inspections done early and selling with confidence, is the clearest path to a smooth closing. Buyers should get both inspections to protect their investment and their financing.

Our perspective: What most buyers and sellers miss about 4-point inspections

Most people treat the 4-point inspection like a bureaucratic hurdle. They schedule it because their insurer demands it, hand over the report, and move on. That mindset costs people real money.

Here is the truth we see on the ground in Baldwin and Mobile Counties: the deals that stall are almost always the ones where a flagged system was ignored or a report lapsed past the insurer’s validity window. A seller who knew their HVAC was aging but didn’t address it before listing is now watching their buyer scramble for coverage three days before closing.

The contrarian view is this: spending money to repair or update a flagged system before the inspection is not a cost, it’s an investment. It speeds up the sale, reduces the risk of a premium surcharge, and removes the single biggest insurance obstacle in coastal Alabama transactions. Reviewing the proper preparation tips before your inspection appointment takes less than an hour and can save you weeks of delays. The 4-point inspection is not a hoop to jump through. It is one of the most actionable pieces of information in your entire transaction.

Need a 4-point or pre-listing inspection? We can help

If you are ready to meet insurance requirements or want peace of mind before selling, local experts have your back.

At Trinity Home Inspections, we serve homebuyers and sellers across Baldwin, Mobile, and surrounding Gulf Coast Alabama counties, including Gulf Shores, Orange Beach, Fairhope, Daphne, and Foley. We are InterNACHI-certified, locally owned, and built on a foundation of honesty and integrity. Our reports are delivered the same day, packed with photos and video, and written in plain English so you know exactly where you stand.

Whether you need a 4-point inspection to satisfy your insurer or a full pre-listing inspection before putting your home on the market, we are ready to help. You can also use our property and permit search tool to research a home’s history before you commit. Reach out today and let’s make sure your transaction moves forward without surprises.

Frequently asked questions

Who usually pays for the 4-point inspection, the buyer or the seller?

Typically, the homebuyer pays as part of their insurance application process, but motivated sellers sometimes cover the cost to remove obstacles and speed up the sale.

How long is a 4-point inspection report valid in Alabama?

Most reports are valid for 1 to 5 years, but the exact window depends on your insurance carrier and whether any major system changes have occurred since the inspection.

Does a 4-point inspection include code compliance?

No. The inspection is a visual condition assessment focused on age, function, and risk, not a code compliance review or enforcement action.

Can a flagged 4-point inspection cancel my real estate sale?

The inspection has no pass or fail, but if the insurer denies coverage based on flagged systems and the buyer cannot secure insurance, the transaction can absolutely fall through.

Are 4-point inspections required for all homes in Baldwin or Mobile County?

They are generally required for homes over 20 to 30 years old in coastal zones, but new construction is rarely subject to this requirement unless a specific carrier mandates it.

Recommended