What Inspectors Check in a 4-Point Home Inspection

- Matt Cameron

- Apr 26

- 10 min read

Updated: Apr 29

TL;DR:

A 4-point inspection focuses on roof, electrical, plumbing, and HVAC systems to determine insurance eligibility.

Insurers use this report to decide whether they will issue or renew a homeowner’s policy, especially for homes 20+ years old.

Proper preparation and understanding of inspection criteria can help prevent coverage delays and streamline real estate transactions.

If you think a 4-point inspection is just a shorter version of a full home inspection, you are not alone. But here is where that assumption can cost you. Insurers across Gulf Coast Alabama use this focused report to decide whether they will cover your home at all. Inspectors examine roof, electrical, plumbing, and HVAC systems only, and the results carry enormous weight. One failed system can block your insurance approval, stall a closing, or give the other party serious negotiating power. If you are buying or selling a home that is 20 or more years old in Baldwin, Mobile, or the surrounding Gulf Coast counties, understanding this inspection is not optional. It is essential.

Key Takeaways

Point | Details |

Focus on four systems | A 4-point inspection only reviews roof, electrical, plumbing, and HVAC—not the whole house. |

Insurance denial risks | Roofs with less than 3 years life, outdated wiring or pipes, and systems in poor repair commonly block insurance approval. |

Visual, fast, and cost-effective | This inspection takes about an hour and costs $100–$250 in Gulf Coast Alabama. |

Documentation is key | Permit records and maintenance documentation make or break report results for buyers and sellers. |

Negotiation leverage | 4-point inspection findings offer powerful bargaining tools for repairs, coverage, and price. |

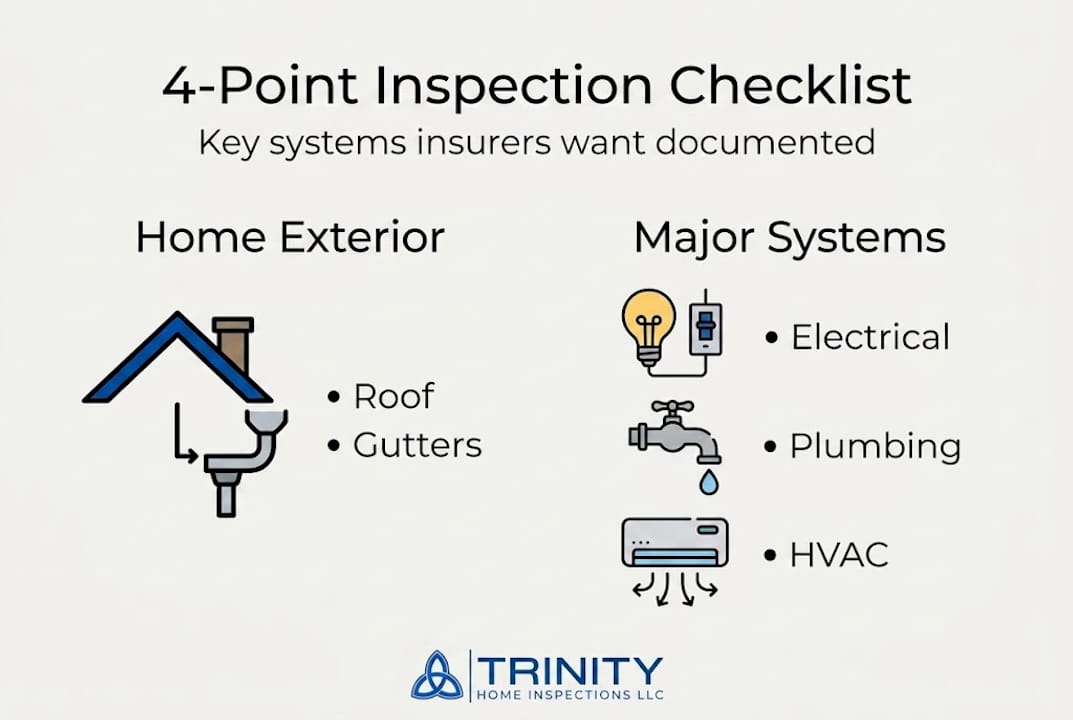

What is a 4-point inspection and when is it required?

A 4-point inspection is a specific, limited evaluation that focuses on four systems in a home: the roof, electrical system, plumbing, and HVAC (heating, ventilation, and air conditioning). Unlike a full home inspection, which covers everything from the foundation to the attic and every accessible component in between, this inspection is narrowly scoped. Insurance companies request it because these four systems represent the greatest risk for large claims.

The inspection is visual and non-invasive, meaning the inspector does not open walls or dismantle equipment. It typically lasts 30 to 60 minutes and costs between $100 and $250 in the Gulf Coast Alabama market. The inspector produces a standardized report that insurers use to evaluate whether a property qualifies for a homeowner’s insurance policy.

Insurers require this report for homes that are 20 to 30 or more years old in Baldwin and Mobile Counties. Coastal proximity raises the stakes even higher. Many insurers in this region will not issue a new policy or renew an existing one without a current 4-point report on file. This makes it a non-negotiable part of the real estate transaction for a large portion of homes in Gulf Coast communities like Daphne, Fairhope, Foley, and Orange Beach.

It helps to understand exactly how this inspection differs from a full assessment before you walk into a transaction. Here is a quick comparison:

Feature | 4-point inspection | Full home inspection |

Systems covered | Roof, electrical, plumbing, HVAC | All accessible systems and components |

Purpose | Insurance eligibility | Buyer due diligence |

Duration | 30 to 60 minutes | 2 to 4 hours |

Cost range | $100 to $250 | $300 to $500+ |

Report format | Standardized insurer form | Detailed narrative with photos |

Required by | Insurance companies | Buyers, lenders (sometimes) |

You can review a detailed 4-point inspection checklist to see exactly what gets evaluated on each system. It is also worth noting that a 4-point report does not replace a full inspection. If you are buying a home, you need both.

Over 60% of homeowner insurance claims trace back to problems with these four systems, which is precisely why insurers built this report around them.

Understanding common inspection findings in Gulf Coast Alabama can help you spot patterns before the inspector ever arrives.

Roof: What inspectors look for and common disqualifiers

The roof is the most scrutinized part of a 4-point inspection, and for good reason. In Gulf Coast Alabama, roofs take constant punishment from heat, heavy rain, and hurricane-force winds. An insurer’s first concern is whether the roof has enough useful life remaining to justify coverage.

Inspectors check age, material, condition, visible damage, estimated remaining life, and permit history during the roof portion. They look for missing, cracked, or curling shingles. They check for signs of active or past leaks, sagging decking, and deteriorating flashing around chimneys, vents, and skylights. The material matters too. Architectural shingles, metal roofing, and concrete tile all carry different life expectancy ratings that insurers factor into their decisions.

Permit records are a critical piece of the puzzle. If a roof was replaced but no permit was pulled, an insurer may treat it as unverified and potentially deny coverage. This is a more common issue in Gulf Coast Alabama than many buyers realize, and it can turn a smooth closing into a prolonged dispute.

Roofs with less than 3 to 5 years of estimated remaining life are frequent triggers for denied coverage or mandatory repair requirements before a policy is issued. Some insurers set their threshold even higher depending on the coastal zone.

Here is how common roof conditions typically affect insurance approval:

Roof condition | Likely insurance outcome |

New or recently replaced with permit | Approved, favorable rate |

5 or more years remaining, good condition | Approved, standard rate |

3 to 5 years remaining, minor wear | May require documentation or repair |

Less than 3 years remaining | Often denied or requires replacement |

Visible major damage or active leaks | Denied pending repair |

Secondary roof layer over existing | Flagged, often denied |

Unpermitted roof replacement | Flagged, requires verification |

Common roof disqualifiers inspectors flag during a 4-point review include:

Multiple layers of roofing materials stacked on top of each other

Unpermitted repairs or replacements without documentation

Visible storm damage such as missing sections or impact marks

Significant moss or algae growth indicating moisture retention

Active leaks or visible water staining on decking

Failing flashing around penetrations

You can learn more about what goes into roof inspection details for Gulf Coast properties, including how age is documented from data plates and county records. If you want to check permit history before making an offer, a permit search in Alabama can reveal whether prior work was properly filed.

Pro Tip: Buyers should pull permit records on any home built before 2005 before submitting an offer. An unpermitted roof replacement can create insurance complications that delay or derail a closing, and that information is often available before you ever schedule an inspection.

Poor drainage around the roofline compounds these issues. Gutter problems on Gulf Coast homes are common contributors to premature roof deterioration, and inspectors take note when gutters show signs of chronic overflow or improper slope.

Electrical, plumbing, and HVAC: Inspection criteria and hidden risks

Once the roof section is complete, the inspector moves to three systems that carry their own set of serious risks for Gulf Coast homeowners. Each one has specific disqualifiers that insurers watch for, and some of them are non-negotiable.

For electrical systems, inspectors evaluate the panel brand, amperage, wiring material, and any visible hazards such as double-tapped breakers, scorching, or exposed wiring. The goal is to assess fire risk. Two panel brands that consistently trigger insurance denial are Federal Pacific and Zinsco. Both have documented histories of breaker failure that create fire hazards. Knob-and-tube wiring, which was common in homes built before 1950, and aluminum branch circuit wiring from the 1960s and 1970s are also major red flags.

For plumbing, major disqualifiers include polybutylene pipes, which were widely used from the late 1970s through the mid-1990s and have a well-documented record of sudden failure. Inspectors also check for galvanized steel pipes, which corrode from the inside out over time. The material, age, and visible condition of supply and drain lines all factor into the report.

For HVAC, inspectors assess age, condition, and life expectancy of the heating and cooling equipment. They look for refrigerant leaks, dirty evaporator coils, and signs of deferred maintenance. A system that is past its expected service life, typically 15 to 20 years for most units, may trigger a request for proof of serviceability or a requirement for replacement.

Salt air and hurricane exposure accelerate wear on all four systems in Gulf Coast Alabama homes. Electrical connections corrode faster. HVAC coils degrade sooner. Roofing materials age more quickly than inland equivalents. These are not theoretical risks; they are realities inspectors see in this region constantly.

Here are major disqualifiers by system:

Electrical:

Federal Pacific or Zinsco panels

Knob-and-tube or aluminum branch circuit wiring

Double-tapped breakers or visible scorching

Panels with insufficient amperage for current loads

Plumbing:

Polybutylene supply lines

Severely corroded galvanized steel pipes

Active leaks or signs of past unremediated water damage

No shut-off valves or improperly installed fixtures

HVAC:

Systems older than 15 to 20 years with no service records

Refrigerant leaks or damaged coil fins

Non-functional heating or cooling at time of inspection

Evidence of makeshift or unpermitted modifications

To prepare your systems before an inspection, follow these steps:

Ensure clear access to the electrical panel, water heater, HVAC unit, and attic.

Gather any available maintenance records for the HVAC system and major plumbing repairs.

Test that all systems are operational before the inspector arrives.

Address any known visible issues such as dripping faucets or tripped breakers.

Confirm that filters are clean and HVAC vents are unobstructed.

You can review the full inspection checklist to see how each system is evaluated in detail. Understanding inspection standards for Gulf Coast properties helps sellers avoid surprises on inspection day.

Pro Tip: Sellers who address flagged electrical, plumbing, or HVAC issues before listing save themselves from last-minute repair negotiations. A pre-listing inspection lets you fix problems on your timeline rather than under closing pressure.

If you want to know what Gulf Coast buyers need to ask before closing, reviewing the right questions to ask inspectors can save you time and money.

The 4-point inspection report: What buyers and sellers should expect

Once the inspection is complete, the inspector compiles the findings into a standardized report that goes directly to the insurance company. This is not a narrative document like a full home inspection report. It is a structured form that answers specific questions insurers need to make a coverage decision.

Inspectors document system ages using data plates on equipment and permit records from county databases. Photos are included for every system and any notable condition. The report also captures estimated remaining life for the roof and HVAC system, pipe materials, and wiring types. Every section is designed to give an underwriter a clear picture within minutes.

The standardized report format is what makes this document useful to insurers. It removes ambiguity. There is no room for vague descriptions when an underwriter needs a yes or no on polybutylene pipes or Federal Pacific panels.

Here is what each section of the report typically contains:

Report section | Key details documented |

Roof | Material, age, estimated life, condition, visible damage, permit status |

Electrical | Panel brand, amperage, wiring type, hazards observed |

Plumbing | Pipe materials, supply and drain condition, visible leaks |

HVAC | System age, condition, estimated life, functional status |

Photos | Visual documentation for each system and flagged items |

Insurers review the completed report and make one of three decisions: approve coverage, deny coverage, or approve coverage with conditions such as a required repair within a set timeframe. Understanding that process helps you plan your next move.

If the report reveals issues, here is how to respond:

Read the report carefully and identify which systems triggered concerns.

Get repair estimates from licensed contractors for any flagged items.

Use the repair costs as negotiating leverage with the seller or buyer.

Request a re-inspection once repairs are documented and complete.

Provide the updated report to your insurance agent before the policy effective date.

You can find more guidance on the home inspection checklist page, and if you are ready to move forward, you can schedule an inspection that fits your timeline.

Clear photo documentation of each system gives buyers real negotiating power. When a report shows a 19-year-old HVAC unit or polybutylene pipes, that evidence turns a vague concern into a documented repair request with real dollar figures attached.

The uncomfortable truth most buyers and sellers miss about 4-point inspections

Here is what we see time and again in Gulf Coast Alabama real estate: people treat a 4-point inspection like a pass-fail quiz, and then they are shocked when the insurer still has questions or declines coverage.

Passing a 4-point inspection means the four systems met a minimum threshold. It does not mean the insurer will offer favorable rates. It does not mean hidden defects do not exist. And it absolutely does not mean the home is ready for the next 20 years without significant investment.

Sellers in older Gulf Coast homes often underestimate edge-case risks. A roof with four years of estimated life might technically pass today. But if closing drags on for 60 days, an insurer can revisit that estimate. A system that sits right on the boundary is not a comfort; it is a liability waiting to surface at the worst possible moment.

Buyers need to think beyond pass or fail. Use the report as a starting point, not a finish line. If the HVAC is 17 years old and barely functional, that is a budget item, not a technicality. If the panel passed but showed signs of overloading, that warrants a closer look from an electrician.

The questions buyers should ask before and after an inspection can reshape how you interpret the findings and how aggressively you negotiate.

Insurance decisions are made in minutes based on these reports. Your preparation matters more than you think.

In this coastal market, where salt air, storm season, and humidity accelerate system wear, the margin between a passing report and a denied policy is thinner than most people expect. The buyers and sellers who come to the table with documentation, maintenance records, and professional inspections already in hand are the ones who close with confidence.

Take the next step with trusted inspections and permit searches

Knowing what a 4-point inspection covers is only useful if you act on it before it becomes a problem at closing. Whether you are a buyer trying to understand your insurance options or a seller who wants fewer surprises, professional inspection and permit verification services give you the clarity to move forward.

[

At Trinity Home Inspections, we serve homebuyers and sellers across Mobile, Baldwin, Escambia, Washington, Monroe, and surrounding Gulf Coast Alabama counties. Our pre-listing inspection service helps sellers identify and address issues before they derail a deal. Our permit search service helps buyers verify whether prior work was properly documented. And our same-day reports, free thermal imaging, and InterNACHI certification mean you get accurate, actionable information without the wait. Explore all of our inspection services for Gulf Coast Alabama and take the next step with a team that treats your transaction with the care it deserves.

Frequently asked questions

How long does a 4-point inspection take in Gulf Coast Alabama?

A typical 4-point inspection lasts 30 to 60 minutes and is visual only, covering just the four key systems without opening walls or dismantling any equipment.

What are the main disqualifiers in a 4-point inspection for insurance?

Common disqualifiers include roofs with less than 3 years of estimated life remaining, polybutylene pipes, aluminum or knob-and-tube wiring, and panel brands such as Federal Pacific or Zinsco.

How much does a 4-point inspection cost in Alabama?

In 2026, costs in the Gulf Coast region typically range from $100 to $250, making it one of the more affordable inspections you will order during a real estate transaction.

Is a 4-point inspection the same as a full home inspection?

No. A 4-point inspection examines only four systems and produces a standardized insurer form, while a full home inspection covers all accessible components of the property and delivers a detailed narrative report.

How can sellers prepare for a 4-point inspection?

Sellers should ensure clear access to all systems, gather available maintenance records, and resolve any obvious visible issues with the roof, electrical panel, plumbing, or HVAC before the inspector arrives.

Recommended